When to take Canada Pension Plan (CPP) paymentsSunday, April 25, 2021

|

||

|

Canada Pension Plan payments are a regular topic of conversation in my office. Not a surprising topic for a financial planner. What is surprising is the variety of recommendations, outcomes and other conversations that happen after the initial CPP topic is raised.

Canada Pension Plan (CPP) is a government-managed pension that is payble to those who have contributed. Contributions happen through employment in Canada- you contribute as an employee (check your pay stub, you'll see a deduction) and your employer contributes on your behalf as well (this is one of the payroll taxes for employers). If you're self-employed, you contribute both sides. The amount of CPP that you receive in retirement is based on your personal work history, subject to annual maximums.

Frequent comment from clients: "I don't think I'll get that; isn't it clawed back?" Answer: No, CPP isn't ever clawed back. It is taxable to you as pension income, but there is no clawback. Old Age Security (OAS), another government retirement income program, IS income-tested, and will be clawed back once an individual exceeds income threshholds.

As a recipient, you have choices in when you start collecting CPP. You can collect as early as age 60, or as late as age 70. Age 65 is considered normal retirement age, and your calculations start from this assumption. For each month that you collect before age 65, you will receive a reduced CPP amount. For each month that you wait to collect after age 65, you will receive a higher CPP amount.

The CPP Take-Up Decision ,released by the Society of Actuaries on July 2020, and widely reported on by media in Dec 2020, comments on a micro-simulation done by the Society to look at possibilities in payment amounts if you delay until age 70. I love research, and I love that this report has sparked conversations. I don't think that delaying CPP until age 70 is the best choice for all clients, or possibly even most clients.

There are many other factors that affect your CPP decision. If you delay, your CPP monthly amount is higher, up to 150% higher than if you started payments at age 65. During the 5 years between 65 and 70, to maintain your available income, you will be using your own assets- RSP/RIF; TFSA; non-registered accounts. This will pull your personal net worth lower until age 70, when CPP starts. Depending on your situation, your personal net worth may start to increase again.

In a plan that I completed for clients in 2020, this is exactly what happened- Milo (not the client's real name) was sure that he wanted to delay payments until age 70. He was aware of the increase, and 150% more seemed too good to pass up. The initial projection using delayed CPP showed a potential net worth at age 95 that was $400,000 higher than if Milo and his wife Jeanettte (also not the client's real name) started payments at age 60. That mattered....the age that these two were starting retirement was at the edge of 60. Not 65, 60. When that happens, your personal CPP calculation includes 5 years of zero earnings- you're not working after all. The report didn't look at how to handle early retirement and years of zero income inclusion. After age 65, there is no income inclusion when it comes to your personal CPP calculation.

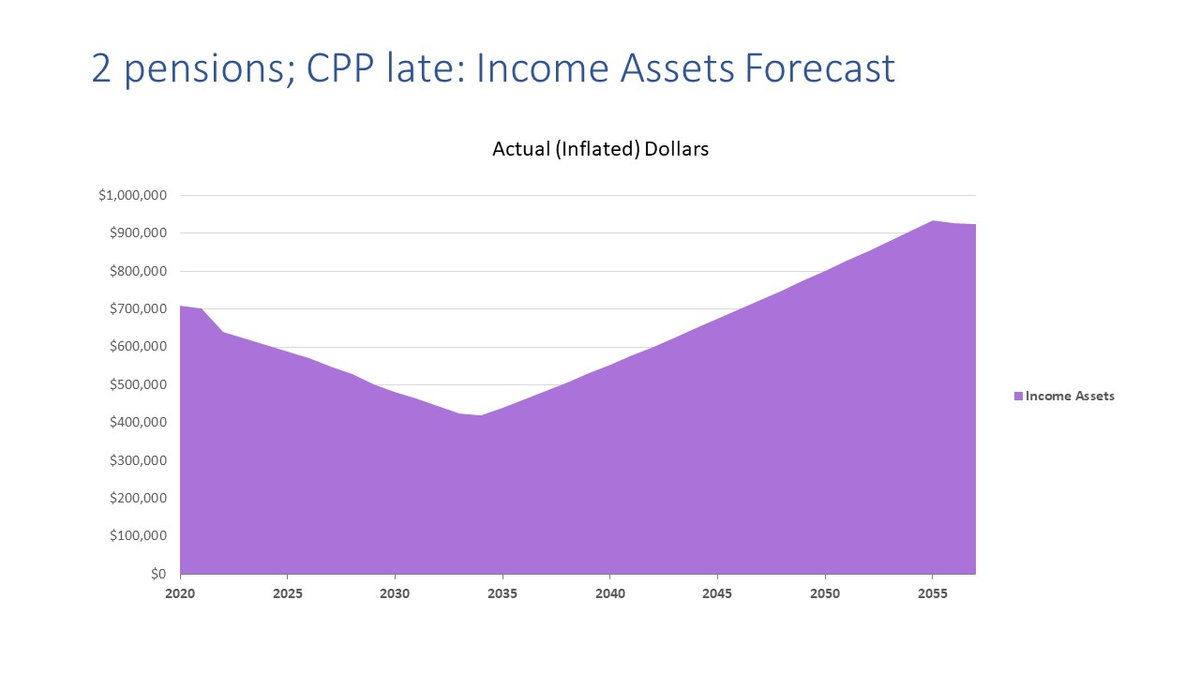

Here's what it looked like for Milo & Jeanette's investment account if they delayed CPP until age 70:

Milo & Jeanette's own investments declined until age 70, when CPP payments meant smaller/no withdrawals from their own investments. This looks fine- ater all, their projected estate value is healthy, there was no reduction in desired income in any years, and more money was coming from the government in the form of higher CPP payments.

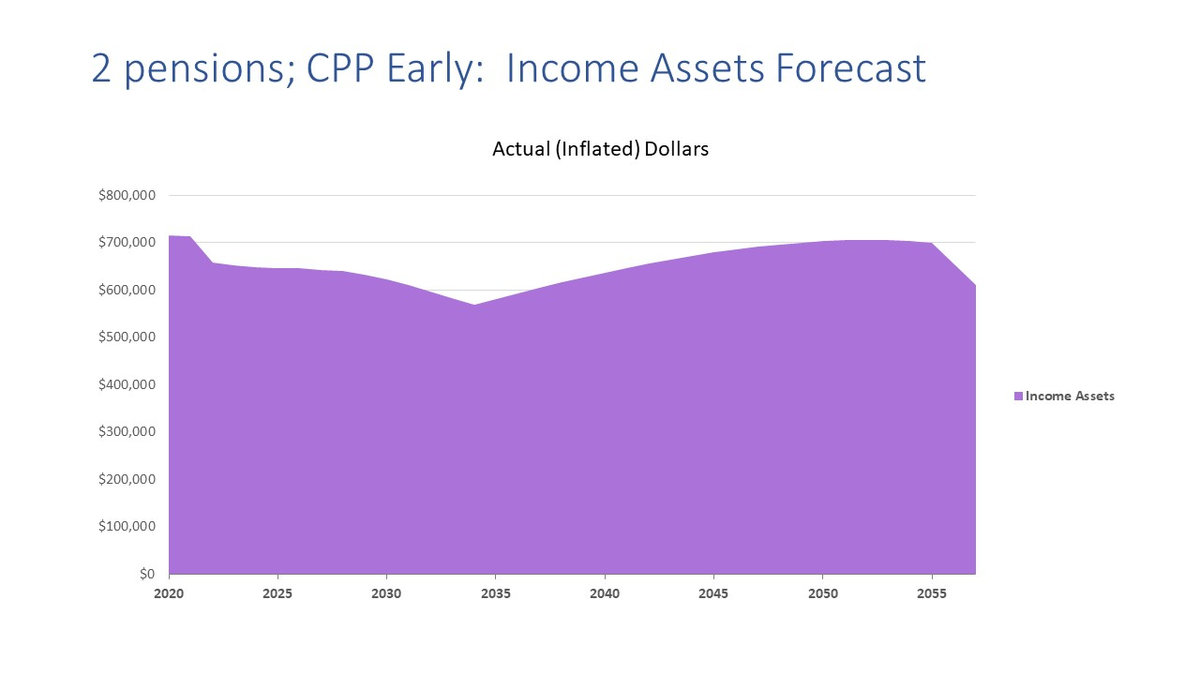

Then we looked at a projection of what could happen if they started CPP at age 60. This means a permanent reduction in the payment amount of 36% (of the age 65 amount).

Overall, this scenario is projecting a lower estate value at Milo and Jeanette's age 95. For some clients, this isn't desirable. Milo and Jeanette didn't want a large estate- leaving money to family wasn't something high on their priority list. Comparing the two graphs allowed for a conversation about the 'risk zone' that happened from age 65 to 75- their own assets were lower, and one of them passed away, the survivor wouldn't receive any more CPP. CPP does have a survivor benefit that is paid to a spouse- but only if that spouse isn't already at the maximum CPP payment amount personally. And the deceased OAS payments would stop as well. The effect of a negative stock market and losing one of them in that 'risk zone' would have had a potentially large impact on the income available to the surviving spouse. This is a decisioin that can only be made by the people it affects. It can't be made at all if the planning isn't done to visualize each scenario.

For many reasons, they left that appointment agreeing that waiting wasn't the automatic best choice for them. One of the beautiful things about CPP is that you can choose to start payments in the month that makes most sense for you between the ages of 60 and 70. You don't have to declare an intention and be held to it. There's flexibility every 30 days in those years. |

||

|

||

|

||

|

||

|

|

|

|

Sara McCullough 98 July 14, 2026 |