Happy 2025!

Want a broad overview of how to think about your finances and set goals for this year?

This article by Srvindhya Kolluru has tips from myself, Blair Lukan and Scott Plaskett.

Your Will and COVID19Wednesday, April 8, 2020

|

||

Your Will and COVID19

COVID19 has moved 'get a will' from the bottom of our to-do list to the top. How to do that legally and while staying at home? Check out this article for guidelines...and a reminder that a handwritten will is good for now, not a replacement for a full document drawn up by an experienced lawyer. One tip the article left out- please let someone know where your will is stored. Contact me if you have questions.

|

||

|

||

|

||

|

Getting and GivingFriday, October 6, 2017

|

||

Getting and Giving

On this Thanksgiving weekend, many of us will have an opportunity to spend time with family and friends. This holiday can be a time to reflect on what we are thankful for, or what we have received. Christmas is only ** days away. Pre-Christmas can be a season of charitable solicitations, a time when many focus on giving to family, friends and charities. Recent Statscan statistics reveal that 84% of Canadians claimed a charitable tax deduction, and 44% of Canadians volunteer their time. Like other areas of your life, taking the time to develop your giving plan can have significant positive impact for you and those that you help. A meaningful giving plan starts with a discussion about what issues you care about and why you want to support them. What does community mean to you? What are your views on international versus local ventures? Answers to these initial questions will drive the rest of the dialogue about where and how to have an impact on issues that matter most to you. A deep discussion about your values will connect your giving to the rest of your plan; income, spending, investments and estate planning will all start to reflect your values about who and how you want to be in your community. To have a conversation that starts with your interests and goals, ending with an executable plan, instead of starting and ending with tax strategies, contact Sara at 519-569-7526 or [email protected]

Places to Go to Stretch Your Thinking:

Questions and Framework to Evaluate Your Giving

Volunteering and Charitable Giving in Canada

An Answer to Some Headlines Generated by the Above StatsCan report

A Journey from Charity and Donors to an Investment Fund

|

||

|

||

|

||

|

Planning for Special NeedsWednesday, September 27, 2017

|

||

Planning for Special Needs

Creating and maintaining a family always comes with unexpected highs and lows. The birth of a child is a joyous event, regardless of the challenges. When a child is born with special needs—whether developmental or medical—parents can face unique challenges that can initially feel overwhelming. When first learning their child has special needs, parents face a steep learning curve, says Kathy Netten, a social worker with the complex care program at The Hospital for Sick Children (Sick Kids) in Toronto. Parents need to learn medical terms, how to navigate the healthcare system and how to advocate effectively. Because many conditions are discovered in infancy, they are often learning how to be parents for the first time. And, they may also be grieving. Sick Kids has over 50 social workers like Ms. Netten who provide counselling, therapy and support services for families with special needs children. “We are available to help parents find resources and work effectively with care teams, to problem solve when there are challenges, and for the very difficult decision-making,” she says. From her experience, Ms. Netten says parents will often push themselves to physical and mental exhaustion to benefit their child. “The key is to find a balance between hope and despair, even under the most difficult of circumstances. Hope will allow parents to take care of their own emotional, psychological and spiritual needs so they can care for the developmental and medical needs of their child.” Parents must also be mindful that financial questions are not forgotten at this most critical time, only to become an additional burden later on. While it can be difficult to think about long-term financial concerns, a firm financial foundation will not only protect your family, it will also free you to focus on the physical and emotional needs that only you can meet. For parents of special needs children, this can be even more important. A typical family will see income increase over time. However, for families with special needs children—especially those that have the most complex needs—literature shows that income actually decreases. Medication and equipment costs, time taken from work, and lack of knowledge of available assistance programs are all contributors. A comprehensive financial plan for families in this situation will:

To review your situation and explore how a personalized plan would benefit your family, please contact Sara at 519-569-7526 or [email protected].

Originally published by Financial Planning Standards Council. Adapted with permission. |

||

|

||

|

||

|

Building Blocks-Wealth TransferWednesday, June 7, 2017

|

||

|

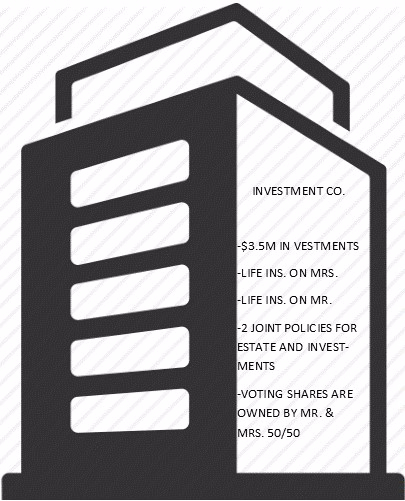

Last week’s blog discussed the difference in outcome when you have a will versus the intestate rules being applied to your estate. Taking our example on step further, what happens when Mrs passes away? Based on our initial example, this family had saved and invested well. Mrs’ career allowed her to maintain the family’s lifestyle without using investments. Investment Corporation is also holding 3 in-force life insurance policies that will pay to the corporation once Mrs passes away. Assuming Mrs lives to her average life expectancy of 83, the estate will be worth approximately $14 million. If she passes sooner, at age 55, the children will inherit approximately $2,500,000 each when they are in their early 20’s. How do you increase the likelihood that your estate will benefit your family/beneficiaries and decrease the potential negative impact of what may be sudden wealth for someone unprepared?

The sooner you have these conversations, the more time you have to repeat the information. Learning happens over time, with repetition. It’s not too late to start talking as a family about your values and how to handle money and wealth so that it meets your goals instead of acting as a hindrance.

Disclaimer- the above example is a hypothetical situation for illustration purposes only and is not to be considered legal advice. Intestate rules vary from province to province. For legal advice specific to your situation, drafting and execution of your wills, please consult your lawyer.

To discuss your current situation and estate goals, please contact [email protected] to book an appointment.

Check in later in June for blogs on how to talk your kids about money and finances.

|

||

|

||

|

||

|

The Importance of having a WillWednesday, May 31, 2017

|

||

|

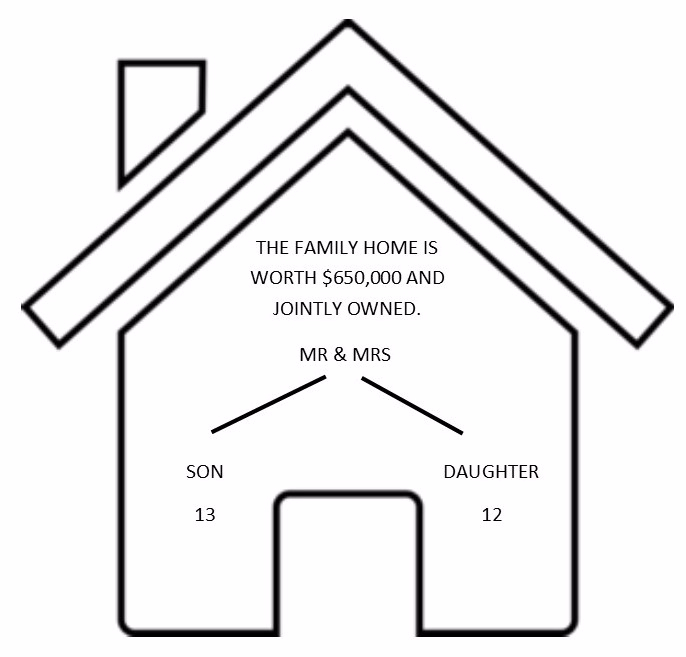

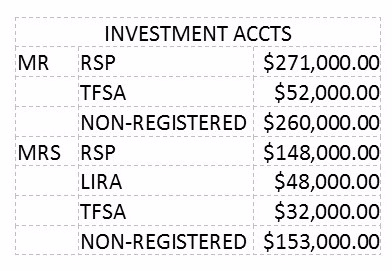

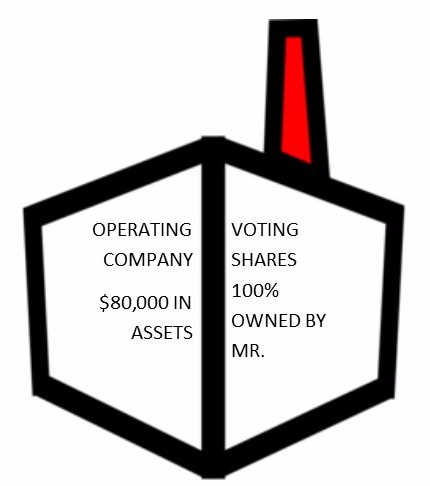

Our Scenario family lives in Ontario. Mr owns Operating Company, which generates approximately $500,000 in revenue per year. He takes $152,000 in salary. Mrs is a professional, earning $180,000 per year in salary. Total family expenses are $120,000 per year.

This seems like a good news story, financially. Careers are stable, living expenses are below incomes, and savings rate is high. Mr and Mrs don’t have wills or power of attorney. They’ve had initial conversations with their investment advisor and with a lawyer. They got stalled in a few questions from the lawyer, and haven’t been back to see her. In Canada, each province has rules for asset division and estate settlement if someone dies without a will. This is known as “intestate”. We may want our surviving spouse to inherit our assets and continue to parent the children with the values we had before our death; without a will, this isn’t what will happen. Mr dies suddenly without a will. After the settlement process, using the intestate laws in Ontario.

Mr dies suddenly, after completing wills leaving his assets to Mrs.

This scenario is not about financial devastation after the loss of an income-earning spouse. Financially, the surviving parent is stable, and can maintain the family’s lifestyle after the loss. This scenario is about loss of financial control, as the children will have access to a significant amount of money in their own names. The loss of financial control is preventable, through executing a will that reflects your values in a legally sound way.

Disclaimer- the above example is a hypothetical situation for illustration purposes only and is not to be considered legal advice. Intestate rules vary from province to province. For legal advice specific to your situation, drafting and execution of your wills, please consult your lawyer. How an Estate may be administered if a minor child has a claim under an Intestate Estate

To discuss your current situation and estate goals, please contact [email protected] to book an appointment

|

||

|

||

|

||

|

|

|

Sara McCullough 83 July 24, 2024 |

|

|

Lindsay Seyler 1 May 10, 2017 |